January 22, 2026

January 22, 2026

Convertible bonds: understanding and optimizing this hybrid financing tool

Convertible bonds are complex but powerful financial instruments, often used by both listed and unlisted companies to meet specific financing requirements. If you're wondering about the interest, functioning or risks of this mechanism, this article will give you all the keys you need to decide whether this type of bond is right for your company or your investor portfolio.

Before going any further, it's important to understand what a standard bond is. A bond is a loan: a company (or a government) borrows money from investors, in exchange for which it undertakes to pay them regular interest (called "coupons"), and then to repay the amount lent at a date fixed in advance. For the investor, buying a bond means lending money in exchange for an income known in advance, with a guaranteed repayment date (unless the issuer defaults).

What is a convertible bond?

A convertible bond is first and foremost a classic bond: a debt security that enables an issuing company to raise funds on the market in exchange for the payment of coupons at a rate fixed in advance. But it differs in one major respect: it offers its holder a conversion right. Under certain predefined conditions, the investor can convert his or her loan into shares in the company.

This means that when you subscribe to this type of loan, you lend money to the company in the same way as with a standard bond, but you have the option of becoming a direct shareholder at maturity. This mechanism combines the security of a debt security with the potential for gain linked to share price performance.

"The convertible bond is a bridge between debt and equity, offering both parties unparalleled flexibility."

Why make this strategic choice when you have good cash flow management? For the company, it is a way to attract capital at a cost that is often lower than a traditional loan, as the conversion option is very attractive to investors. For you, it is an opportunity to secure a return while retaining an option on the company's growth. It is therefore important to monitor your cash flow movements.

ℹ️ Example: Let's imagine an unlisted tech company wishing to finance its growth without immediately diluting its founders. It issues a 5% convertible bond over 5 years. If the company succeeds, the share price rises, and investors can convert their bonds into shares at a price fixed in advance, thus realizing a potential capital gain. If not, they simply get their capital back, plus the expected coupon.

Characteristics of convertible bonds

Convertible bonds differ from other forms of securities in several respects:

- Lifespan: generally 3 to 7 years, but can vary according to business needs.

- Interest rates: fixed, variable, indexed or revisable, offering the flexibility that appeals to institutional investors seeking diversification.

- Issue price: must be at least equal to the par value of the shares received on conversion.

- Redemption: in most cases, the principal is repaid at maturity, unless the bond is converted into shares.

- Redemption premium: paid only if the bond is not converted at maturity.

- Early redemption option: the company can sometimes redeem the bonds before maturity, thus capping the investor's capital gain.

To subscribe to a convertible bond, you need to fully understand the issue contract, which sets out all conversion terms, exchange ratios and redemption scenarios.

What are the risks and returns of a convertible bond?

For the holder of a convertible bond, the return is twofold:

- A fixed portion: the coupon, which is often lower than that of a traditional bond.

- A random component: the potential capital gain linked to conversion, capped in the event of early redemption.

For the issuing company, this is the assurance of finding lower-cost financing with a deferred dilutive effect. However, the risk of conversion failure, linked to a possible fall in the share price, is assumed by the company.

Why choose a convertible bond?

Are you wondering why so many companies choose to issue convertible bonds rather than a traditional loan or a capital increase? There are many reasons, but the financing options too. Let's take a closer look at the advantages and limitations of this model!

Benefits

- Flexibility: adapt to liquidity needs or capital structure optimization.

- Lower cost: lower interest rate thanks to conversion premium.

- Attractiveness: attracts investors looking for yield and potential capital gains.

- Deferred effect on dilution: current shareholders retain control until the bonds are converted.

Limits and risks

- Potential dilution: if the conversion takes place, the share capital is increased, diluting the shareholding of existing shareholders.

- Risk of capital loss: if the share price falls or stagnates, conversion is not attractive, and the investor does not benefit from potential capital gains.

- Complexity of the issue contract: requires legal and financial expertise.

Before resorting to complex instruments such as convertible bonds, many entrepreneurs prefer a quick business loan to finance a crucial stage in their development.

Here are a few points to keep in mind:

- Check the conversion ratio (number of shares obtained for one bond).

- Analyze early redemption clauses.

- Study the issuer's rating, if available.

- Assess the bond's liquidity on the secondary market.

ℹ️ Case study: In 2023, a French industrial SME raised 10 million euros via a convertible bond issue to modernize its equipment. Thanks to the confidence of investors, the company was able to negotiate an interest rate of just 3%, compared with 5.5% for a conventional loan. After three years, half of the bonds had been converted, limiting the debt to be repaid and strengthening the company's equity.

Convertible bonds on the market: practicalities

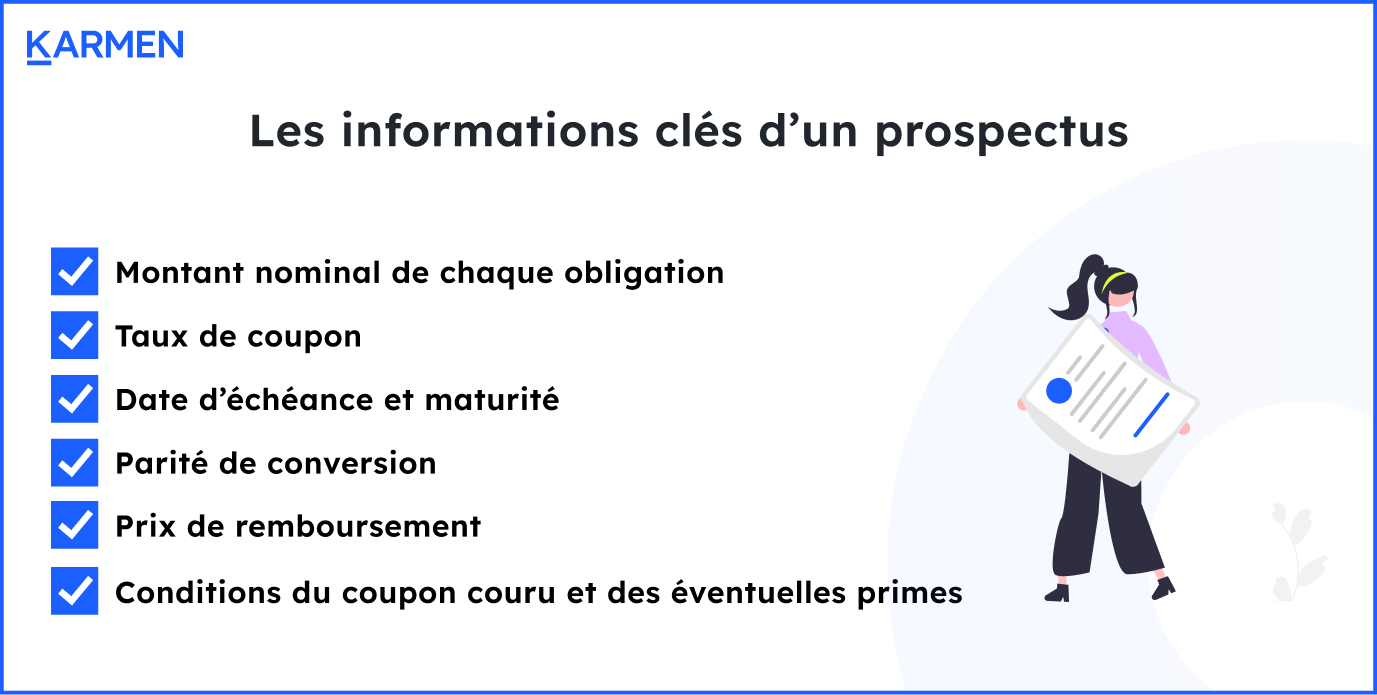

The company wishing to issue convertible bonds may be a large corporation already listed on the stock exchange (such as Euronext), or an unlisted SME. But before it can offer these bonds to investors, it must first obtain the approval of its shareholders at a special meeting called an "extraordinary general meeting", and then draw up an official document, known as a prospectus or contract of issuance, which explains in detail all the "rules of the game". This document serves to inform and protect investors, so that they know exactly what they're getting into. It contains the following terms and conditions:

Convertible bonds are negotiable securities, sometimes listed, and can be bought or resold on a secondary market, offering the holder a degree of liquidity.

A few additional concepts to optimize your strategy

To optimize the use of, or investment in, a convertible bond, several concepts need to be taken into account:

- Convexity: the sensitivity of the bond price to both interest rates and changes in the underlying share price.

- Share premium: difference between the price of the bond and its face value.

- Market rates and interest rate trends: the attractiveness of a convertible bond also depends on the macroeconomic context (inflation, rising interest rates, volatility).

- Diversification: incorporating convertible bonds into a portfolio allows you to diversify between debt and equities, taking advantage of capital protection and upside potential.

You might ask yourself: is a convertible bond suitable for all types of investor? The answer depends on your appetite for risk, your investment horizon and your knowledge of the markets.

Finally, if you prefer more delegated management, certain convertible bond mutual funds or funds allow you to invest in a diversified selection of these securities, benefiting from the expertise of professional managers.

The flexible Karmen Loan financing solution

We launched Karmen Loan to offer companies a flexible, non-dilutive financing solution, ranging from €30,000 to €5 million over terms of 1 to 24 months. This solution is particularly suited to companies wishing to finance their cash flow, inventories, marketing or operational growth without disrupting their capital structure.

Unlike a convertible bond, Karmen Loan gives you quick access to resources without dilution and with great ease of implementation. You retain complete control over your business and benefit from a solution tailored to your operating cycles.

Discover our free guide to financing levers :

Conclusion: convertible bonds, yes, but with caution and discernment

Convertible bonds remain a popular hybrid financing solution, capable of meeting a wide range of needs for both issuer and subscriber. It combines the security of debt with the potential of equity, but requires in-depth analysis of all its features and of the contract under which it is issued.

Before taking the plunge, ask yourself the right questions: how much dilution can you handle? What are your objectives in terms of return and risk? Have you considered all the alternatives on the financing market?